The exponential rise in the national debt since COVID began by the tune of more than $3.8 Trillion of stimulus monies was inevitably going to lead to a wave of hard asset inflation as well as consumer inflation. The only question was "how much"?

The exponential rise in the national debt since COVID began by the tune of more than $3.8 Trillion of stimulus monies was inevitably going to lead to a wave of hard asset inflation as well as consumer inflation. The only question was "how much"?

In the last couple of days, the markets woke up to the fact that inflation might be worse than the federal reserve predicted. The CPI (Consumer Price Index) numbers released for April 2021 rose 0.8% versus an expected rise of 0.2% month over month. Should we be alarmed and worried? In the short term, the answer is "not really". If you have been tracking first quarter earnings calls, you will have heard many CEO's describing how tight supply chains are right now. Higher costs of raw material inputs are being passed onto the consumer. As COVID restrictions ease and consumer demand for goods and services rise alongside tight supply chains operating on "just in time" demand cycles, the natural consequence of greater demand and tight supplies is higher price increases.

It is difficult to say how inflation numbers will fare over the coming months as it will take time for supply chains to re-calibrate and meet rising demand. However, as this occurrs, inflation numbers will likely decrease as supply increases. Overall, however, we expect the inflation trend to show up as net higher consumer prices across most hard and soft asset categories, compared to before the pandemic.

... Joe Biden announced his new trillion dollar infrastructure plan last week and how he intends to fund it, which sent chills through the markets and the $400,000 plus annual income earners. Of course, this should not have come as a surprise. The odds of the Biden Administration not implementing such a key campaign promise was close to zero. What the announcement did do was sound the alarm ammong the top segment of american earners that it was time to take action and evaluate steps to mitigate taxes going forward under the likely scenarios outlined by the president.

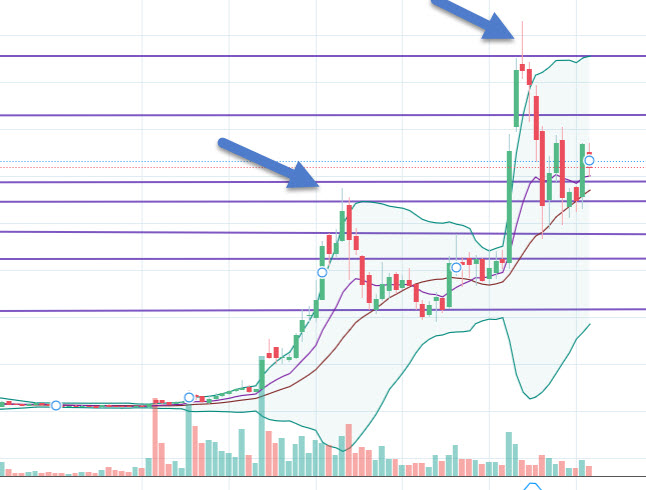

Joe Biden announced his new trillion dollar infrastructure plan last week and how he intends to fund it, which sent chills through the markets and the $400,000 plus annual income earners. Of course, this should not have come as a surprise. The odds of the Biden Administration not implementing such a key campaign promise was close to zero. What the announcement did do was sound the alarm ammong the top segment of american earners that it was time to take action and evaluate steps to mitigate taxes going forward under the likely scenarios outlined by the president. This week, we are going to continue with our "key technical indicators" series for stocks or any publicly traded instrument for that matter. Today, we are going to explore "Bollinger Bands".

This week, we are going to continue with our "key technical indicators" series for stocks or any publicly traded instrument for that matter. Today, we are going to explore "Bollinger Bands"..jpg) Over the coming months we will discuss a variety of stock indicators and how these can help an investor identify market cycles and significant shifts in market or company fortunes. Investors have different time horizons which can vary from 1 day to 30 years. Regardless of the investment timeframe, you must determine an entry and exit price which may or may not sync with your investment timeframe.

Over the coming months we will discuss a variety of stock indicators and how these can help an investor identify market cycles and significant shifts in market or company fortunes. Investors have different time horizons which can vary from 1 day to 30 years. Regardless of the investment timeframe, you must determine an entry and exit price which may or may not sync with your investment timeframe. China has issued a digital Yuan and it's got governments around the world scared and in catch-up mode. So what's the big deal? The world is moving at breakneck pace to a digital based currency system. Cash is being phased out. Consumers around the world are paying increasingly with debit and credit cards. Cash is being used less and less and this trend has only accellerated since the advent of COVID. It only makes sense in a predominantly digital commerce world that this would be accompanied by government issued digital currencies.

China has issued a digital Yuan and it's got governments around the world scared and in catch-up mode. So what's the big deal? The world is moving at breakneck pace to a digital based currency system. Cash is being phased out. Consumers around the world are paying increasingly with debit and credit cards. Cash is being used less and less and this trend has only accellerated since the advent of COVID. It only makes sense in a predominantly digital commerce world that this would be accompanied by government issued digital currencies.